So, what exactly is gap insurance? Think of it as a financial safety net. It’s designed to cover the difference—the “gap”—between what your car is actually worth and the amount you still owe on your loan if it’s declared a total loss.

Simply put, if your main insurance payout doesn’t cover your entire loan balance after an accident, gap coverage steps in to handle the rest. This protects you from getting stuck with a hefty bill for a car you can no longer even drive.

Understanding the Basics of Gap Insurance

Picture this: you just drove your shiny new MINI off the lot here at Habberstad MINI in Huntington. The second those tires hit the street, its value starts to dip. That’s depreciation, and while it’s a totally normal part of owning a car, it can create a serious financial headache early on in your loan.

Your standard collision and comprehensive insurance policies are set up to pay out the car’s Actual Cash Value (ACV) if it’s totaled or stolen. The ACV isn’t what you paid for the car; it’s what the car is worth at the moment of the incident, after factoring in all that depreciation. And that’s where the trouble often starts.

The Financial Gap You Could Face

If you owe more on your loan than the car’s ACV, you’re “upside-down,” and a gap exists. After a total loss, your insurance company will write a check for the ACV, but you’re still on the hook for the remaining loan balance.

This isn’t some rare, worst-case scenario. It’s incredibly common. In fact, up to 85% of new car buyers find themselves owing more than their car is worth during the first few years of their loan. For drivers across Long Island, this is precisely why Guaranteed Asset Protection (GAP) insurance is so important. The demand for this protection is surging, with the global market expected to nearly double from $4.5 billion to $8.8 billion by 2035, which you can read about in reports on the GAP insurance market growth.

To make this crystal clear, here’s a quick breakdown of the key terms.

Gap Insurance at a Glance

| Term | What It Means for You | Example |

|---|---|---|

| Actual Cash Value (ACV) | The amount your insurance company says your car was worth right before it was totaled, including depreciation. | Your new car cost $30,000, but after a year, its ACV is only $22,000. |

| Loan Balance | The total amount you still owe to your lender, including interest. | After a year of payments, you still owe $27,000 on your auto loan. |

| The “Gap” | The difference between your loan balance and your car’s ACV. This is the amount you’d have to pay out of pocket. | $27,000 (Loan Balance) – $22,000 (ACV) = $5,000 (The Gap). |

In essence, gap insurance is like a financial airbag for your auto loan. It ensures you’re not left making payments on a car that’s sitting in a salvage yard. You can settle the old loan and focus on what really matters: getting back on the road.

How Gap Insurance Works in a Real-World Scenario

Theory is one thing, but let’s walk through a real-life example to see exactly how gap insurance can be a financial lifesaver.

Picture this: you’ve just driven off the Habberstad MINI lot in a brand-new MINI, the perfect vehicle for navigating Long Island with the family. The total price tag is $42,000.

You put $2,000 down and finance the rest—$40,000—over a 72-month loan. For the next year, you enjoy your new ride and make every payment on time.

The Total Loss Event

Fast forward one year. You’re cruising down the I-495 when another driver makes a mistake, causing a major accident. The most important thing is that everyone is okay, but your beautiful Telluride is totaled. Your insurance adjuster confirms it’s a total loss.

This is where the numbers get tricky. After a year of payments, you’ve chipped away at your loan and now owe the bank $35,500.

But here’s the catch: cars depreciate. They start losing value the second you drive them off the lot. Your standard auto insurance policy doesn’t care what you paid or what you owe; it only covers the car’s current market value.

Calculating the Insurance Payout

Your insurer does their assessment and determines the Actual Cash Value (ACV) of your one-year-old Telluride is now just $30,500. They’ll cut a check for that amount, but it goes straight to your lender, not you.

So, what happens next? Let’s break down the math:

- What You Still Owe: $35,500

- What Insurance Pays (ACV): $30,500

- The Financial “Gap”: $5,000

That’s right. Even after your insurance pays out, you’re still on the hook for a $5,000 loan balance on a car that’s now sitting in a scrapyard. That’s a painful bill to pay for a vehicle you can no longer drive.

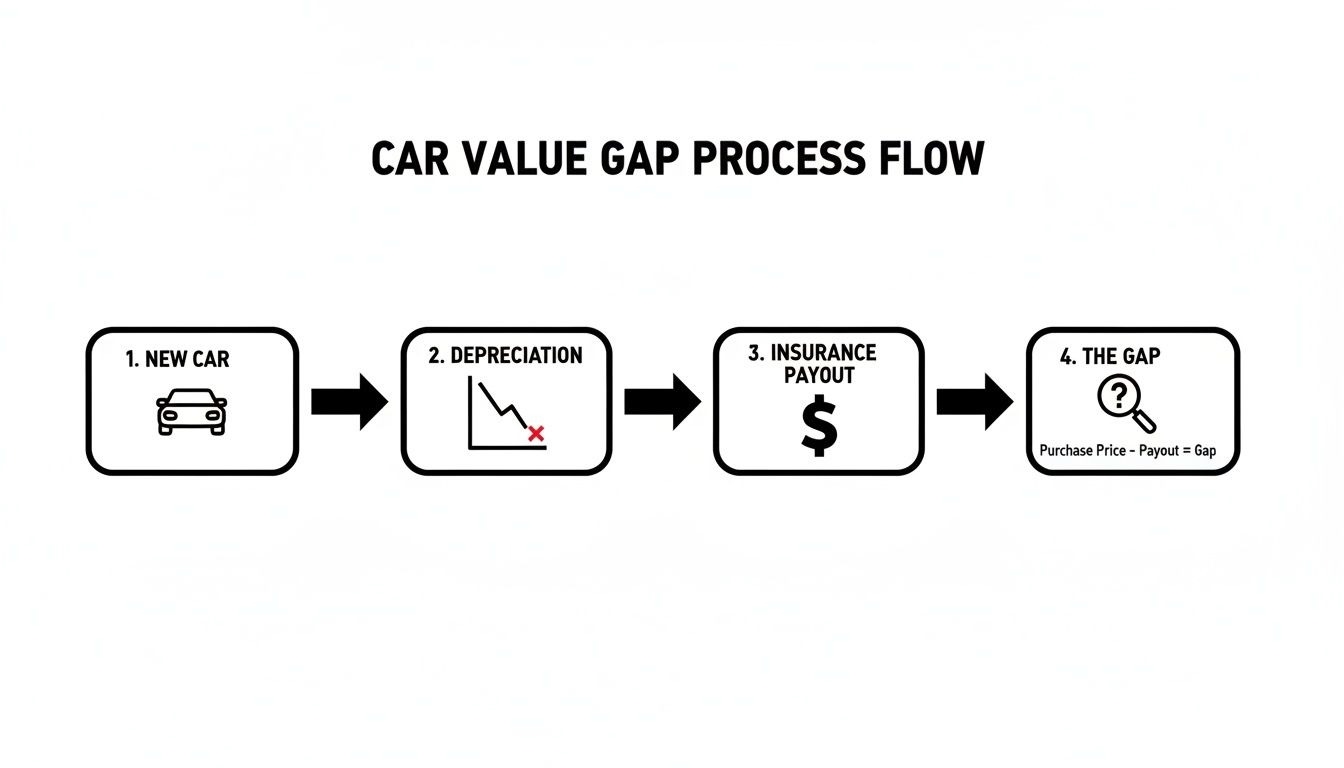

This diagram shows you exactly how that gap appears over time.

As you can see, the gap between what you owe and what the car is worth can grow quickly, leaving you exposed if an accident happens.

How Gap Insurance Saves the Day

But let’s rewind. Luckily, when you bought the Telluride, you had the foresight to add a gap insurance policy.

Instead of getting a bill for $5,000, you simply make a claim. Your gap insurance provider steps in and pays the entire $5,000 difference directly to your lender.

Just like that, the old loan is gone. You’re completely free from that debt.

Now, you can focus on the important stuff—like finding your next car—without the financial ghost of your old loan haunting you. It’s a perfect illustration of how gap insurance acts as a critical financial safety net, protecting both your investment and your peace of mind.

When Do You Actually Need Gap Insurance?

So, how do you know if gap insurance is right for you? It’s not so much about the specific car you’re driving around Long Island, but more about the financial details of your purchase. Certain financing choices can almost guarantee you’ll be “upside-down” on your loan for a while, and that’s precisely when gap insurance becomes a financial lifesaver.

If you’re looking at your auto loan and nodding along to any of the situations below, you should seriously think about adding gap coverage to your policy. It’s a small price to pay for major peace of mind.

Key Scenarios Where Gap Insurance Is a Must

Think of gap insurance as a non-negotiable part of the deal if you find yourself in one of these common spots:

- You Made a Small Down Payment (Less Than 20%): If you put less than 20% down, you’re starting out with very little skin in the game. A new car can lose more than 20% of its value in the very first year. Do the math—that small down payment means you’re almost guaranteed to be upside-down from day one.

- You Stretched Out Your Loan Term (60 Months or More): Longer loans of 60, 72, or even 84 months are pretty common now because they keep monthly payments down. The catch? You build equity at a crawl. Your loan balance shrinks incredibly slowly while your car’s value plummets, creating a huge gap for years.

- You’re Leasing a Vehicle: This one is simple—most lease agreements flat-out require gap insurance. When you lease, you’re not building any equity. If that car gets totaled, you’re on the hook for the rest of the lease payments. Gap coverage is designed to wipe that debt clean.

The question of what is gap insurance for cars is more relevant than ever. Post-pandemic supply chain chaos caused new car prices to soar by 40% from 2020 to 2023. This created an even bigger, more immediate gap between what people owed and what their cars were worth. You can dive deeper into these market trends over at Insurance Asia.

- You Bought a Car That Depreciates Quickly: Let’s be honest, some cars just lose value faster than others. Luxury sedans and certain high-end models are notorious for this. If you bought a vehicle known for taking a steep value hit right off the lot, gap insurance is your shield against that rapid depreciation.

At the end of the day, deciding on gap coverage is a straightforward risk assessment. Look at your down payment, the length of your loan, and the type of car you chose. If there’s a good chance you’ll owe more than the car is worth for the first few years, gap insurance is an incredibly smart, low-cost way to protect your wallet.

Understanding the Cost and Coverage of Gap Insurance

So, you’ve figured out when you might need gap insurance. But what about the nitty-gritty details? Let’s talk about the two most important questions: how much does it actually cost, and what does it really cover? Getting clear on these points helps you see its true value and avoids any nasty surprises down the road.

The price tag for gap insurance can swing quite a bit depending on where you get it. If you tack it onto your existing auto insurance policy, you might only be looking at an extra $20 to $40 per year. It’s a pretty small add-on.

On the other hand, if you buy it from the dealership or your lender, it’s typically a one-time product that costs a few hundred dollars. More often than not, this amount just gets rolled right into your car loan, so you pay for it over time.

Of course, the final cost hinges on a few things: who you buy it from, your vehicle’s value, and how long your loan term is. A pricier car or a longer loan usually means a bigger potential “gap” to cover, which nudges the premium a bit higher.

What Gap Insurance Actually Covers

At its core, gap insurance has one very specific job. It’s designed to pay off the remaining balance of your auto loan after your regular insurance company pays out the Actual Cash Value (ACV) of your car if it’s totaled or stolen.

Think of it this way: gap coverage is the financial bridge that spans the canyon between what you still owe on your loan and what your car is actually worth at the time of the loss. Its only goal is to make you whole with your lender, so you aren’t stuck paying for a car you can no longer drive.

This single function is what delivers such incredible peace of mind. It wipes the slate clean on your old loan, letting you focus on finding a new car without being haunted by the debt from your last one.

But it’s just as crucial to understand what gap insurance doesn’t do.

What Gap Insurance Covers vs What It Does Not

Gap insurance is a specialist, not a jack-of-all-trades. It’s built to tackle a very specific financial risk, and a standard policy has some clear boundaries. Knowing what’s in and what’s out sets the right expectations from day one.

Here’s a quick breakdown to make it crystal clear.

| Typically Covered ✅ | Typically Not Covered ❌ |

|---|---|

| The “gap” between your loan balance and the car’s ACV | Your primary auto insurance deductible |

| Extended warranties or other add-ons rolled into your loan | |

| Late fees or penalties from missed loan payments | |

| Any down payment you made on the vehicle | |

| Costs related to engine failure or mechanical breakdowns |

To put it simply, gap insurance is there to settle your original loan—that’s it. It won’t pay your deductible, cover missed payments, or refund money for other products you decided to finance. Understanding these limitations is the key to seeing exactly where it fits into your financial safety net.

Where to Get Gap Insurance on Long Island

Okay, so you’re sold on the “why” behind gap insurance. The next question for any Huntington or Long Island driver is pretty simple: where do I actually buy it? You’ve got a few solid options, and the best one for you usually boils down to what you value more—convenience or cost.

You can typically find this coverage in three main places: the dealership’s finance office, your bank or credit union that’s handling the loan, or your current car insurance company. Let’s break down what each one looks like.

Your Dealership’s Finance Center

This is hands-down the easiest route. When you’re buying your car at a dealership, the finance manager can offer you a gap policy right then and there. They’ll just roll the cost right into your auto loan.

The beauty of this is its simplicity. Everything is handled in one transaction, and the cost is just a small part of your single monthly car payment. For many people financing a new MINI or another great car, not having to make another phone call or shop around is a huge win.

Auto Lenders and Insurance Companies

Your other options involve a little more legwork but can often save you some money. You can usually buy gap coverage directly from the bank or credit union that’s financing your car. Just ask them when you’re setting up the loan.

Most people, however, find the best rates by calling their own auto insurance provider. Adding gap coverage to an existing policy is often incredibly affordable—sometimes just a few extra dollars on your monthly premium. The only catch is that it’s a separate step you have to remember to take after you’ve bought the car.

Consider this: A Long Island driver finances a new MINI from Habberstad MINI in Huntington with a modest 10% down. With new vehicles losing 20-30% of their value in the first year alone, a significant gap appears instantly. For MINI owners, gap coverage from the dealership often bundles seamlessly with a lease, protecting them from theft or a collision on a busy road like I-495. To see more about the growing need for this coverage, explore insights on the Guaranteed Auto Protection market.

So, what’s the right call? It really depends on you. If you want a one-stop-shop experience, get it at the dealership. If you’re looking to find the absolute lowest price, a quick call to your insurance agent is probably your best bet.

Answering Your Top Questions About Gap Insurance

Alright, let’s wrap this up by digging into the questions we hear most often from drivers around Long Island. Getting the right answers can make all the difference in deciding whether gap coverage is a smart move for your new MINI.

Is Gap Insurance Required When I Lease a Car?

Nine times out of ten, yes. When you lease, you’re essentially renting the car long-term, not building any ownership stake. The leasing company is on the hook if the car gets totaled, so they need to protect their asset.

That’s why most lease agreements have a clause making gap insurance mandatory. You might not even notice it as a separate charge; it’s often rolled right into your monthly payment. Think of it as a standard, non-negotiable part of the deal that ensures the lease is paid off if the worst happens.

Will Gap Insurance Pay for My Deductible?

This is a great question, and it’s a super common misunderstanding. The straightforward answer is no—a standard gap policy won’t cover your regular insurance deductible. Its one and only job is to bridge the financial gap between what you still owe on your loan and what the insurance company says your car is worth.

Now, some dealerships or lenders might offer a premium version or a separate product that does help with the deductible. You absolutely have to ask about this directly. Always read the fine print to see exactly what you’re paying for before you sign anything.

Your gap policy is there to make the bank happy, not to cover your out-of-pocket expenses like a deductible. Get clarity on your specific coverage terms.

Can I Cancel My Gap Insurance Later On?

You bet, and you absolutely should! Gap insurance is only valuable as long as you’re “upside-down” on your loan. The second your car is worth more than what you owe, that “gap” disappears, and you’re just throwing money away on a policy you can no longer use.

You can cancel the coverage at any point. Just call up whoever you bought it from—your insurance agent, the dealership, or the lender—and tell them you want to end the policy. If you paid for it all upfront when you bought the car, you’re usually entitled to a prorated refund for the time you didn’t use.

Ready to find the perfect MINI and protect your investment with smart financing? The team at Habberstad MINI is here to walk you through every step of the process. We’ll make sure you leave our Huntington lot feeling totally confident in your purchase. Explore our new and pre-owned inventory and get expert advice today.